FAQ: How Much Can OVA Dues Finance?

The purpose of this article is to provide some facts concerning how much OVA could borrow as a function of dues impact and other factors (interest, term, etc). It does not address how difficult it might be for OVA to find a lender, or whether or not such a loan should be considered.

Specific questions to be answered:

- For a $10 million loan amount, what would be the loan service cost for different loan terms and interest rates?

- For a $10 per member per month loan service amount, how large of a loan could be financed?

- Once the current large OVA loan is paid off, how large a new loan could be financed without raising dues, i.e. by using the same loan service amount as is currently being incurred for the large loan?

- How large of a loan could be financed without exceeding the 20% annual dues increase that would mandate an OVA membership vote?

All of these questions can be answered using any of the mortgage calculators, along with OVA-specific numbers, but not everyone wants to go through the tedium of doing so. For this article, OVA-specific numbers I am using are:

- Number of dues paying OVA members: 4,700 (this is approximate)

- 2025 OVA dues = $128.50 per member per month

- Current loan service burden:

$625,126 per year = $52,094 per month

$52,094 per month / 4,700 = $11.08 per member per month - For reference, per member per month relative to 2025 dues:

10% = $12.85, 15% = $19.28, 20% = $25.70

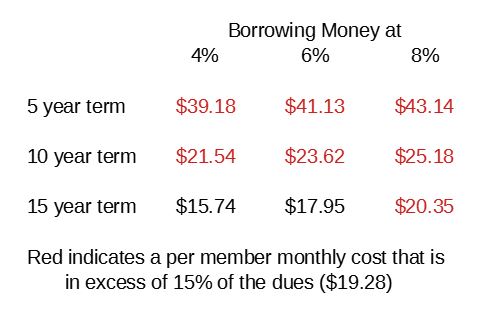

1. For a $10 million loan amount, what would be the loan service cost for different loan terms and interest rates? Table 1 shows the monthly cost per OVA member of servicing a $10 million loan, for terms of 5, 10 and 15 years, and interest rates of 4%, 6% and 8%. As shown in the table, if the term of the loan was 15 years, the cost of servicing the loan would be less than 15% of the current dues amount unless the interest rate was close to 8%. This means that the OVA Board could borrow $10 million and increase the dues in order to make the monthly payments, without having to submit to a vote of the OVA membership. (Note: 15% was used, instead of the statutory 20% threshold, to allow 5% of the annual dues increase to account for inflation in other OVA expenses.)

Table 1. Loan service cost per OVA member per month for $10 million

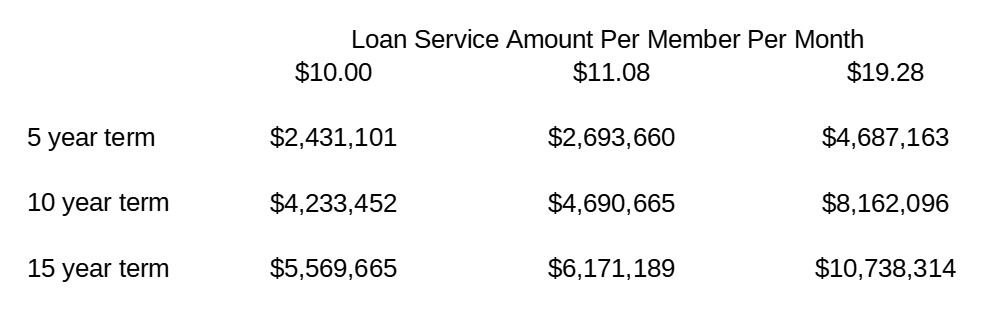

2. For a $10 per member per month loan service amount, how large of a loan could be financed? Table 2 shows the maximum amount that could be borrowed at 6% interest for various loan service amounts. The $10 column answers this question for 5-year, 10-year and 15-year terms.

Table 2. Maximum loan amount for a loan service cost of $10, $11.08 or $19.28 per OVA member per month.

3. Once the current large OVA loan is paid off, how large a new loan could be financed without raising dues, i.e. by using the same loan service amount as is currently being incurred for the large loan? Loan service on the current (East Rec plus golf courses) loan is $11.08 per member per month. Table 2, in the $11.08 column, shows the maximum amount of money that could be borrowed for this loan service amount, for 5-year, 10-year and 15-year terms.

4. How large of a loan could be financed without exceeding the 20% annual dues increase that would mandate an OVA membership vote? A 15% was used, instead of the statutory 20% threshold, to allow 5% of the annual dues increase to account for inflation in other OVA expenses. As noted above, 15% of the 2025 OVA dues is $19.28 per member per month. Table 2, in the $19.28 column, shows the maximum amount of money that could be borrowed for 5-year, 10-year and 15-year terms with a 15% increase in dues used for loan service.

Finally, note that if you want to know how much might be financed if the current loan were retire AND dues were increased by 15%, then you could add together the amounts in the $11.08 and $19.28 columns of Table 2.

Caveats: Nothing mentioned in this article is intended to imply that there is any current plan by OVA to borrow additional money for any reason. This article also does not make any value judgement concerning whether or not loans should be used for any OVA purpose. It merely sets out the limits on how much could be borrowed under several assumptions, and how much dues would have to be increased if the OVA Board decided to use loans to finance construction or purchase of buildings, or for any other purpose.

Bruce, a very interesting analysis. On reflection, a couple of factors might reduce these numbers somewhat. First, the loan fees or cost of issuing the loan or bond (in the case of, say, a taxable bond). Usually those are drawn from the amount financed, reducing the net cash out. The second is a bit harder to estimate, but could cause a bigger reduction. That is the matter of the quality of the credit, in other words, how likely are the revenues promised in repayment likely to actually be available. Maybe someone already knows the answer to this, as the loan for the purchase of the golf course was underwritten using basically the same source: monthly payments from residents of Oakmont. The one possible fly in the ointment: what if a fire swept through and burned some or all of the residences? Some bond underwriting in the single-family housing market will discount the payment stream by up to a third. Don’t know how this works out, but something to keep in mind.

Thanks for this analysis Bruce.